There’s something that’s always been strange to me. If you and I are under the same insurance — shouldn’t we care about each other’s health? Everyone’s money basically goes into a pool and is redistributed to whoever needs it (minus administration costs, etc.). But if we could keep EACH OTHER healthier, then savings could be reinvested back into the community — which is anyway the premise of member-owned health insurance plans like HCSC.

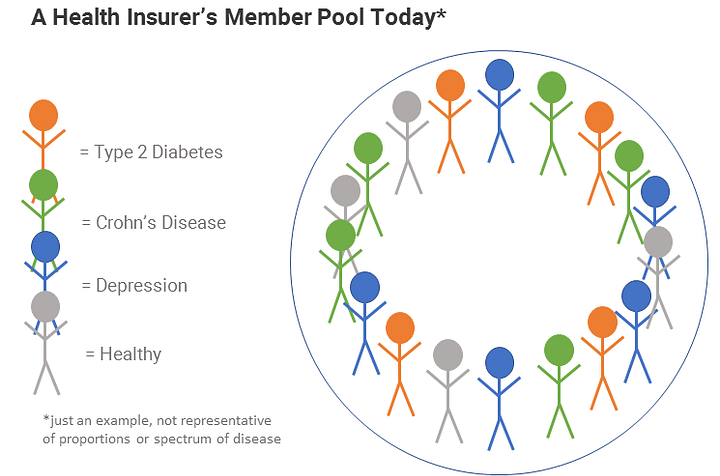

But health insurance currently isn’t set up for us to help each other. When you sign up for an insurer’s plan like Aetna or UnitedHealth, you’re thrown into a massive pool with other nameless customers, with the risk and cost spread across everyone.

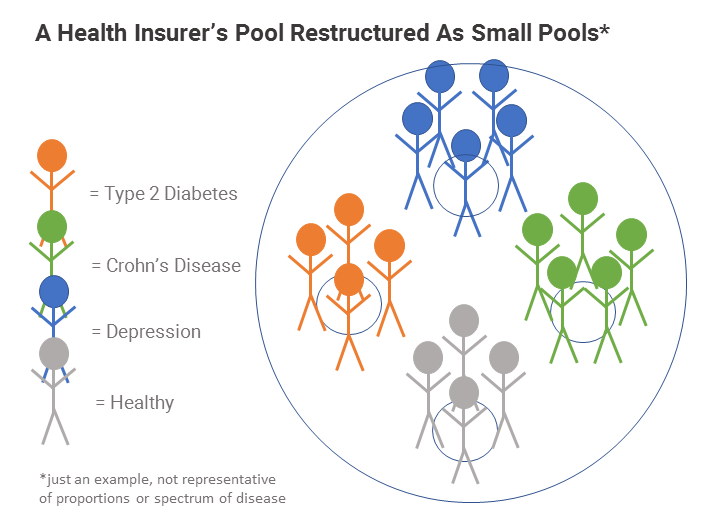

I’m proposing something slightly different. What if instead of one large pool alone, an insurer actually grouped everyone into small pools that rolled up INTO their large pool and you were actually connected with people like you?

To be clear — this isn’t discriminating based on disease type, but figuring out the best ways to manage conditions AFTER you’ve signed up for an insurer. It’s the same group of people for the insurer, but they’re just structured differently internally. I understand that an insurance company with only a high-risk pool would end up in the optimistic sounding “death spiral”.

Small-pool restructuring might look something like this:

- You sign up for a health insurer’s plan.

- You’re put into a group of 10 with people who have similar health profiles as you (age, family history, existing disease, etc.) and therefore relatively similar health goals. Identities would be anonymous by default, but opt-in to reveal more personal information.

- There are individual health goals given to you and then group goals for all 10 to reach. This would include primary care check ups, fitness goals, screenings, etc.

- A dual reward system exists for hitting personal goals and group goals. Many of the member-owned health plans emphasize the re-investment of their earnings back into the community — this could provide a tangible reinvestment avenue that’s theoretically transparent to members and a good marketing tool to get people interested.

Small pool insurance a new dimension: peer accountability and peer support. These two concepts have completely changed other industries by commoditizing trust, unlocking supply, and incentivizing good behavior — but we’ve barely seen this in health insurance. Here’s what small group insurance could potentially do:

- Make people more proactive about their health and encouraged/held accountable by peers instead of just personal accountability.

- Gamify health & wellness goals.

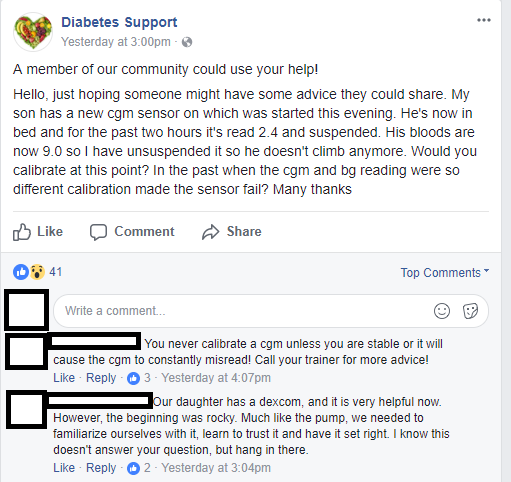

- Distribute knowledge that’s been built up by people with specific conditions e.g. diabetics giving diet tips, advice on how to navigate the system and specialists to see, etc. This creates a scalable way for insurance to complement their existing support systems. We’re seeing this happen on sites like PatientsLikeMe and more informally on forums and Facebook groups.

- Create communities — especially important when it comes to mental health as a co-morbidity to make other problems worse. Medicare patients who live alone, for example, could benefit greatly from virtualized communities.

- Increase stickiness — more investment into a community means the more likely a person will want to stay in that community.

- Provide more personalized support, services, and coverage based on the group. Some of the disease specific plans like Leap Diabetes give a sense for what this might look like.

There are a lot of obstacles to a system like this, including but not limited to:

- What if people don’t want to share their health information at all, de-identified or not?

- Is peer accountability even enough to get people to care about their health?

- What happens when someone develops a new condition? Do they get shifted from one group to another?

- Won’t people still just be switching in and out of health insurance plans if they change employers or move? Doesn’t that ruin the “community” aspect of it?

My hunch is that an idea like this is enabled by tech to do the segmentation, customized incentives, tracking, and interaction between members. However it still largely requires a shift in behavior and regulation before it could become a reality.

Perhaps the more realistic implementation for this would be for the existing online communities, i.e. PatientsLikeMe, to handle the grouping, community aspects, and accountability systems while insurance companies handle the back-office parts (financing, claims processing, etc.). Eventually those platforms could bundle the leverage of their aggregate user base to move upstream and become their own carriers (a strategy I’ve talked about previously in “Tech-Enabled Leverage”). Or maybe this is the model of an entirely new health insurance carrier that’s dedicated to a model like this.

I have no idea if this is a viable idea or even a better one than the existing system, but it’s one I think it’s interesting enough to get thoughts about. Let me know how wrong I am in the comments or on twitter @nikillinit.