Table of Contents

- Two-Way Advocates

- Healthcare and CPG

- ACA Native Businesse

- Overguarded Patient Info

- Areas I See Opportunity

There are too many middlemen “two-way” advocates in the health system

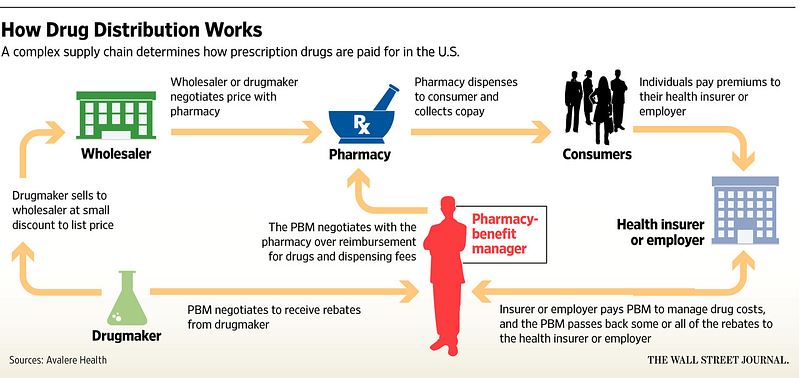

As I started researching more into the health system, I actually became more confused the more I learned. I could not understand how certain companies could act in the best interest of both the patient and any of the other actors in the health system. Patients want to reduce their expenses but everyone else in the health system sees that expenditure as revenue. So when massive institutions exist to benefit both the patients AND one of these other actors, I get very confused at how that’s possible. The best example I can think of this are PBMs (Pharmaceutical Benefits Managers), which I’ve talked a bit abouthere and there. Here are where PBMs fit in:

First of all who needs this many nodes in the supply chain anymore? This is what pre-internet commerce looked like, there’s no reason our pharmaceutical system should be different.

But the crux of the problem happens where the two lines point directly at the PBM (insurer/employer pays PBM, and drug companies give PBM rebates). Take this recent commentary on Mylan (maker of Epipens):

The intermediaries, including wholesalers and pharmaceutical benefits managers, or PBMs, are key players in deciding which drugs get used and how much they cost patients. While the rebate amounts are usually kept under wraps for competitive reasons, the case of EpiPen is offering a rare insight into how the system works — and the blame game resulting from it. Drugmakers say the price increases fund ever-rising rebates, while PBMs say costs would be even higher if they didn’t negotiate the discounts on behalf of insurers and employers.

“The PBMs say things like ‘It helps us keep our prices low to our customers,”’ [Wells Fargo analyst David Maris] said of rebates. “But that’s not what’s going on, it’s part of their business model now.”

PBMs are offered rebates from drug companies, but we don’t know the amount for any of these negotiations? And we’re supposed to believe that the middleman is passing these cost-savings to patients? How does that make any sense?

Similarly, the relationships between providers and med device/pharma companies can be very gray. As a patient, we put full faith that a doctor is acting full in our best interest to get the best care for the lower price. But if the doctor is incentivized to push certain products, how can a patient without medical knowledge discern this? Look at how Medicare reimbursement for cancer drugs currently works:

The proposed Medicare pilot will fundamentally change how doctors are reimbursed for giving chemotherapy and other injectable drugs. Currently, doctors are paid by a simple formula: the average sales price of the drug, plus 6 percent (under the federal budget sequester, that amount has been cut to 4.3 percent). That means doctors see a bigger upside when they prescribe and administer the most expensive drugs. Under the pilot, doctors will receive an amount far less influenced by the drug’s price: a flat fee, plus 2.5 percent of the price (0.9 percent under the sequester).

The fee-for-service system as a whole looks like this, and takes advantage of the expertise asymmetry between doctors and patients. It’s a problem if we can’t trust that our doctor is working in our best interest.

Many healthcare products have CPG (consumer packaged goods) characteristics

Considering that a big part of Obamacare was giving patients more power when it came to purchasing decisions, a bigger opportunity around patient-targeted branding seems to exist, and for some sections of healthcare that looks very similar to some of the newer disruptive CPG models. Think about Unilever/Procter and Gamble who spend billions on television advertising, sell relatively commoditized products, and subsequently saw disruption via companies with stronger branding, new business models, and that lived closer to the consumer.

Many products in healthcare fit a similar profile – low risk products that are relatively undifferentiated and a doctor would feel comfortable allowing the patient to make that choice. Since many health products follow some sort of schedule, the subscription aspect also works well. Product profiles that fit this description are things like prescription skin cream, male baldness, contacts, diabetic products, etc. which have the opportunity to build strong consumer facing brands and have potential patients advocate for their products.

CPG investors typically avoided this because of healthcare affiliations, and health investors typically avoided this because it was less based on defensible tech/formulation/etc. But now the lines seem to be blurring.

Affordable Care Act “native” businesses

Alex Danco wrote another great series about “paradigm shifts”. When new technologies emerge/shifts in systems happen, many successful companies build natively into those system and understand the inherent advantages of the shifts (I recommend reading the whole series since it’s too difficult to summarize here). But it helps to explain why legacy businesses that try to simply “tack on” new ideas or technologies have a harder time than companies that do it from the get-go.

In healthcare’s case the paradigm shift is both digital technologies and value-based care. But should we be shocked that it’s taking longer than we expected to see results? We’re talking about multi-billion dollar businesses where the systems and fee-for-service incentives were built and thrived pre-ACA, and we expect wide spread changes to happen less than a decade later in a system that almost diametrically opposes the previous system? The internet was around in the 90’s but took a decade plus to really start seeing potential. It’s been even less time than that and healthcare is harder to disrupt due to regulation, more entrenched incumbents, higher switching costs, and generally slower, more risk-averse participants.

In the wake of the laggard response for healthcare giants to react to the fee-for-value shift, are there companies that are built natively in the ACA + high technology era? Most companies I see try to shave dollars off of certain inefficient processes in the current health system, but that only further embeds the problems of the prior system. Malay Gandhi wrote a great piece about this, with a very powerful conclusion:

Rather than trying to improve them, the most exciting health tech companies will ignore the parts of healthcare that have become obviously anachronistic, actively discarding convention. The seeds of this difference have been sown in a handful of companies started in the last few years. They are painstakingly taking relationships from incumbents, winning with deflation, and making healthcare markets more efficient. A different healthcare system will inevitably be created.

The companies that I think will hit larger strides of success are the ones that build entirely new systems outside of the current healthcare track with the principles of preventive medicine and digital technologies at the core of the business instead of a tack-on. Companies based on tech principles like asynchronous communication to scale down costs (eg. Lemonaid Health andNurx) or using tech to bundle leverage (eg. Blink Health) fit this new paradigm well. The new standalone health insurance companies where the value premise is keeping people healthy and out of hospitals in the long run (where tech plays a big part in that strategy) are also good examples (Oscar,Clover, etc.). However, they also prove how capital-intensive and difficult it is to fight against the existing system with Oscar going through many shifts itself. It’s not like tech where a shift in user-behavior can generate massive influence in a couple of years. Healthcare is more complex, regulation heavy, and deals with a way more precious resource than attention, which is life itself.

Patient information is unnecessarily overguarded and overblown

The internet and social media has all but eliminated privacy. Most people make the tradeoff understanding that they give up their privacy in exchange for convenience, connection, and a general improvement in their well-being.

Yet in healthcare that same tradeoff is stigmatized. Fear created around the sanctity of patient data, exacerbated by HIPAA and sensationalist headlines have warped people’s perspective on their health data. The reality is more information can be discerned from a person’s credit card statement and their online activity than their health data (especially when the ACA prevents denial based on previous conditions anyway). On top of that 3rd party companies can still get your data.

The people who stand to gain the most from HIPAA are the ones whose business actually works better thanks to data blockages and lackluster interoperability in the system (EMRs, HIPAA consultants, etc.). The ones who lose from it are patients, physicians, researchers, and society as a whole.

I mean c’mon, the original law was written in 1996 with some addendums and attachments slapped on through the years. A societal shift or two might have happened in the last 20 years, the law should be gutted and patient data shouldn’t be put on the pedestal that it is. People should be educated in what’s actually important about their health data and how they can choose to opt-in to programs that might benefit them in exchange for the use of their data (ie. recruitment to relevant clinical trials, having your information easily available when you visit different specialists, etc.)

*Note: One critical piece of data in health records is your Social Security Number, which is a piece of information we’re comfortable giving in many other instances (banks, real estate, etc.) and is more an issue of how secure the data is by the system than the type of data itself. Due to legacy IT systems and poor monitoring, health systems are a vulnerable target.

Areas I’m Interested In/See Opportunity

A few areas I’m particularly interested in reading/learning more about (or better yet, if you’re doing work in any of these spaces let‘s chat).

Genetic Counseling: As the price of gene sequencing goes down and more people begin to get their own genome sequenced, massive datasets are going to be created. Many people are focusing on the cutting and analysis of data, but further than that I think we’ll start to see more and more services built around this information, especially in the form of genetic counselors who can explain to patients what their data means and how to plan around it. As of a few months ago, there were a total of 4,000 certified genetic counselors, a ratio of 1:80,000 for people in the US.

New Patient Identification Systems: As I said earlier, one of the most important pieces of information in your health data is your SSN. Replacing that with a different type of identifier in all non-core parts of your healthcare would not only help to unify your health data across different siloes but might also make that piece of your data more protected. This is one area I could see blockchain playing a big role, or companies like CrossChx are building their own methods.

Voice/Chat UIs: I think for the most part standalone chatbot and voice businesses have a very tough road when it comes to competing with the big tech companies. I think healthcare presents an exception due to the fact that these companies don’t have access to the datasets. A voice/chat interface could unify many of the disparate backend processes that plague healthcare and turn them into accessible tools for the consumer. And accessibility generally leads to transparency since it brings to light many of inconsistencies in things like pricing. Voice could play a particularly crucial role considering the many situations doctors/surgeons are hands-free and the vast amount of information that’s transmitted orally in hospitals (there’s an entire industry of medical scribes that pretty much exist to convert voice into text data).

Autonomous Vehicles/On-Premise Wearables: Both of these have an opportunity for the same reason: hospitals can actually set up their own ecosystems that don’t have to interact with the outside world. Robots that carry medical supplies can navigate hallways and bring them where they need to be or be set up in labs to conduct the mechanical parts of experiments (making the experiments reproducible in the process). Wearables can help track patient vitals/movement, create biometric based security measures internally, and also help understand behavior within hospitals themselves. A health system represents an enterprise opportunity where people are essentially siloed within an area, making it a great testing ground for different types of hardware.

If anything I wrote in my stream of consciousness resonates with you, please reach out to me on twitter @nikillinit, and I’d love to hear your thoughts.